The Surplus Conversion Engine™

They earn well. They save something. They open investment accounts. They read the books. They have good intentions, a spreadsheet somewhere, and a vague sense that they are “doing the right things.”

And yet, years pass.

Net worth grows slowly.

Financial freedom still feels far away.

Nothing truly compounds.

Nothing scales.

Nothing produces enough income to reduce their dependence on work.

This is one of the most misunderstood stages of wealth creation.

A surgeon earning $600,000 can remain financially dependent.

A business owner earning $180,000 can become financially independent.

The difference is not income.

The difference is conversion.

Income is raw material.

Surplus is potential.

Capital is activated potential.

And only capital can compound into assets, systems, time, and eventually freedom.

That is the missing mechanism between earning well and becoming truly wealthy.

I call it the Surplus Conversion Engine™.

The Builder’s Plateau

This is the stage where income has grown, the career is working, the household looks successful, and there is usually money left over.

But freedom still feels distant.

The person is no longer struggling to earn.

They are not living paycheck to paycheck.

They may even have investments.

But they are still highly dependent on their own labor.

They cannot step away.

They cannot slow down.

They cannot make major life decisions without considering the income consequences.

They are successful, but not yet free.

This is the Builder’s Plateau.

And the problem is rarely discipline.

It is rarely intelligence.

It is rarely access to investment opportunities.

The problem is architecture.

The Builder stage is defined by surplus: the gap between what you earn and what you spend.

But surplus without a destination does not automatically become capital.

It becomes lifestyle creep.

It becomes scattered investments.

It becomes upgrades.

It becomes idle cash.

It becomes the “investment opportunity” someone mentioned at lunch.

It becomes financial drift that feels like progress but is not.

The Builder stage has a specific failure mode:

Reactive allocation.

Money arrives.

Then life absorbs it.

A little goes to the mortgage.

A little goes to the vacation.

A little goes to the renovation.

A little goes to a random investment.

A little stays in checking.

A little disappears into subscriptions, convenience, and unexamined lifestyle expansion.

Nothing feels reckless.

Nothing feels catastrophic.

But the result is clear:

High income.

Low conversion.

Thin capital base.

Continued dependence on work.

That is not a character flaw.

That is a systems gap.

Surplus Is Not Wealth

One of the central ideas in Financial Alchemy is this:

Surplus is not wealth. Converted surplus is.

Surplus is only the possibility of wealth.

It is the raw material.

It is the ore before refinement.

It is the seed before planting.

Capital is what surplus becomes after it has been captured, separated, protected, and assigned a purpose.

This distinction matters because many high-income professionals confuse having money left over with building wealth.

They are not the same thing.

Money left over can sit.

Money left over can leak.

Money left over can be consumed.

Money left over can be redirected by urgency, emotion, or opportunity.

Capital is different.

Capital has a job.

Capital is organized for compounding.

Capital is deployed into assets.

Capital is the fuel that eventually buys back time.

This is the Financial Alchemy sequence:

Income → Surplus → Capital → Systems → Time → Freedom

Most people try to leap from income directly to freedom.

They assume that if they earn enough, freedom will eventually appear.

But freedom is not produced by income alone.

Freedom is produced by a sequence.

Income must become surplus.

Surplus must become capital.

Capital must enter systems.

Systems must produce value without your constant effort.

Only then does time begin to return to you.

And only when time returns do you begin to experience true financial freedom.

This is why earning more is not always the answer.

More income without conversion simply creates a larger lifestyle.

More income with conversion creates a larger capital base.

The difference compounds over time.

The Surplus Conversion Engine™

It is not a budgeting technique.

It is not willpower.

It is not a savings goal written in a notebook.

It is the system that moves a person from Builder to Investor.

Its purpose is simple:

To convert income into capital consistently enough that compounding becomes inevitable.

Not occasionally.

Not when motivation is high.

Not when markets look attractive.

Not when there is money left at the end of the month.

Every month.

Every quarter.

Every year.

For decades.

Most people focus on investments.

Investors focus on conversion.

Because compounding does not work on income.

Compounding works on capital.

The question is not simply:

“How much do I earn?”

The better question is:

What percentage of my income becomes capital?

That question changes everything.

The Three Installs

The Surplus Conversion Engine runs on three components.

Think of them as the software installed into your financial operating system.

Install 1: The Conversion Rate

The first question every Builder must answer is:

What percentage of my income becomes capital?

Most people track income.

Investors track conversion.

Income measures production.

Conversion measures wealth creation.

A professional earning $250,000 and converting 25% into capital will often build more wealth than someone earning $500,000 and converting 5%.

Why?

Because markets do not compound your salary.

They compound your capital.

Your conversion rate is the percentage of earnings that consistently becomes future assets.

Not vacations.

Not lifestyle upgrades.

Not parked cash.

Not money that might be invested later.

Capital.

A conversion rate is not a vague intention to “save more.”

It is a number.

It is written down.

It is automated.

It is reviewed.

It is protected from monthly negotiation.

The Builder’s job is not only to earn more.

The Builder’s job is to convert more.

Plain language version:

Before you pay the world, pay your future. Pick a number. Lock it in. Stop renegotiating with yourself every month.

Install 2: The Capital Container

Once surplus exists, it needs a destination.

This is where many Builders fail.

Money without a destination usually finds consumption.

It may not happen immediately.

It may not look irresponsible.

But over time, surplus that remains too close to daily spending is almost always absorbed by daily life.

Investors solve this with a Capital Container.

A Capital Container is a dedicated place where converted surplus accumulates for future deployment.

It could be an investment account.

A brokerage account.

A retirement account.

A real estate opportunity fund.

A business acquisition account.

A corporate investment account.

A holding company structure.

The specific container depends on your stage, country, tax structure, and strategy.

But the principle is universal:

Never leave surplus homeless.

Your capital needs a room of its own.

It should be separate.

It should be named.

It should receive money automatically.

And it should have a clear purpose.

“I’ll transfer it later” is not a container.

It is a good intention.

And good intentions do not compound.

Plain language version:

Open the account. Name it. Automate the transfer. Move the capital before discretion can interfere.

Install 3: The Governance Cadence

Even excellent systems drift without oversight.

This is why Investors install governance.

Governance sounds complicated.

It is not.

Governance is simply a scheduled rhythm for reviewing the system.

Not daily.

Daily checking usually creates anxiety, not strategy.

Not never.

Neglect allows the system to drift.

The right cadence is simple:

Monthly: confirm the transfer happened.

Quarterly: review the rate, container, allocation, and progress.

Annually: audit the entire system and recalibrate for your current stage.

The monthly review can take five minutes.

The quarterly review may take an hour.

The annual audit may require deeper work with your spouse, advisor, accountant, or coach.

The purpose is not to micromanage.

The purpose is to keep the engine aligned.

Your governance cadence should answer four questions:

What was my conversion rate?

How much capital was created?

What assets were acquired?

What systems are beginning to produce cash flow?

What gets reviewed improves.

What gets ignored deteriorates.

Your wealth is a business.

And businesses have operating rhythms.

Plain language version:

Schedule meetings with your own money. Put them in the calendar. They are not optional.

The Compressed 30-Day SCE Installation

You do not need to overhaul your entire financial life in one weekend.

You need to install one engine.

The goal of the next 30 days is not perfection.

The goal is architecture.

One rate.

One container.

One cadence.

That is enough to begin.

Week 1: Measure

Goal:

Know your actual numbers.

For the first week, do not optimize anything.

Just measure.

Identify your monthly income.

Identify your fixed expenses.

Identify your variable spending.

Identify your actual surplus.

Then calculate your current conversion rate.

The key question:

What percentage of income currently becomes capital?

Not savings.

Not money that sits temporarily.

Not money you hope to invest later.

Capital.

By the end of Week 1, you should know:

your monthly income,

your monthly spending,

your monthly surplus,

your current conversion rate,

and your target conversion rate.

Awareness comes before architecture.

Week 2: Build

Goal:

Create the Capital Container.

Now give your surplus a destination.

Open or designate a dedicated account for capital.

Name it clearly.

Examples:

Capital Account

Freedom Fund

Investment Capital

Asset Acquisition Fund

Future Ownership Account

The name matters because it gives the money an identity.

Money called “extra” gets spent.

Money called “capital” gets treated differently.

By the end of Week 2, you should have a separate container that is not mixed with daily spending.

The rule:

Capital must live somewhere consumption cannot easily reach it.

Week 3: Automate

Goal:

Remove monthly decision-making.

This is where the system becomes real.

Set an automatic transfer into the Capital Container.

Ideally, the transfer happens close to payday, before discretionary spending expands to absorb the surplus.

Automation matters because manual systems eventually fail.

You should not have to decide every month whether your future matters.

The decision has already been made.

By the end of Week 3, your conversion rate should be operating automatically.

The rule:

If the system depends on willpower, it is not yet a system.

Week 4: Govern

Goal:

Install the operating rhythm.

Schedule three recurring reviews.

Monthly: five-minute capital confirmation.

Quarterly: one-hour allocation review.

Annually: full SCE audit.

During the monthly review, ask:

Did the transfer happen?

Did the capital reach the container?

Did anything interrupt the system?

During the quarterly review, ask:

Is the conversion rate still appropriate?

Is the container still correct?

Is capital being deployed wisely?

Are we moving closer to the next Financial Alchemy stage?

During the annual review, ask:

Am I still a Builder?

Have I become an Investor?

Does my system need to evolve?

By the end of Week 4, the SCE should no longer be an idea.

It should be installed.

The SCE One-Page Checklist

Conversion Rate

I know my monthly surplus.

I know my current conversion rate.

I have selected a target conversion rate.

My conversion rate is written down.

My transfer is automated.

Capital Container

I have a dedicated capital account.

The account is separate from daily spending.

The account is named for its purpose.

Surplus has a destination before it arrives.

The container has a deployment strategy.

Governance Cadence

I have a monthly wealth review scheduled.

I have a quarterly allocation review scheduled.

I have an annual SCE audit scheduled.

I track capital created.

I track assets acquired.

I know whether I am operating as an Earner, Builder, Investor, or Owner.

Where the SCE Fits in the Financial Alchemy Path

The Surplus Conversion Engine is powerful because it solves a specific problem at a specific stage.

It is not the whole wealth system.

It is the bridge between Builder and Investor.

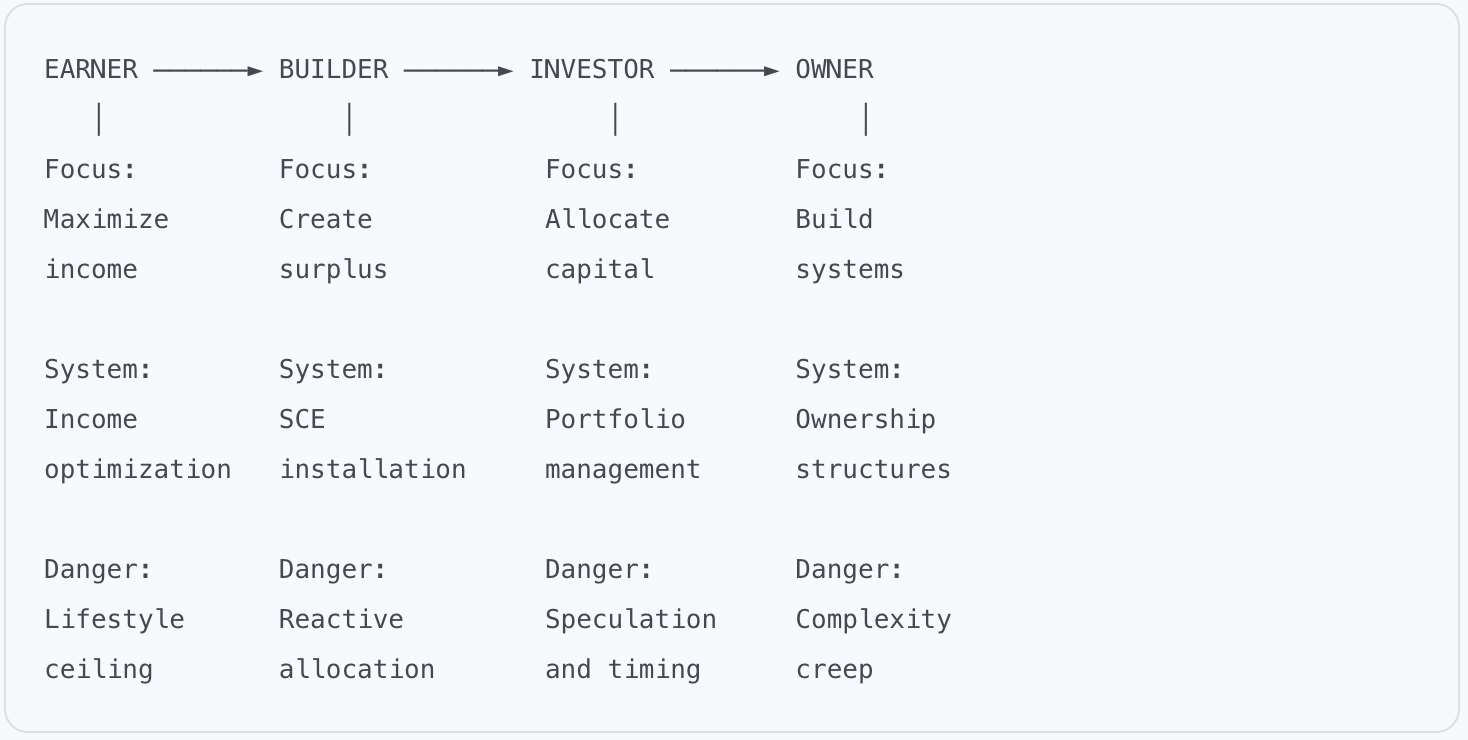

The Financial Alchemy path has four major stages:

Earner → Builder → Investor → Owner

The Earner focuses on income.

The Builder focuses on surplus.

The Investor focuses on capital allocation.

The Owner focuses on systems, equity, and freedom from direct effort.

Each stage has a different question.

The Earner asks:

How do I earn more?

The Builder asks:

How do I keep and convert more?

The Investor asks:

How do I compound more?

The Owner asks:

How do I create freedom from my effort?

The danger is using the wrong system at the wrong stage.

An Earner does not need a complex portfolio strategy before income is stable.

A Builder does not need more random investment opportunities before surplus is reliably converted.

An Investor does not need to keep obsessing over savings hacks after capital allocation becomes the main game.

And an Owner must eventually move beyond personal accumulation into systems, structures, and assets that operate without constant personal labor.

The SCE belongs to the Builder stage.

It is the system that turns a high-income professional into a true Investor.

Without it, surplus leaks.

With it, capital forms.

And once capital forms, compounding can finally begin.

The Final Reframe

Many people believe they have an investment problem.

Most actually have a conversion problem.

They are searching for the next ETF, stock, real estate deal, private investment, tax strategy, or business opportunity.

But the more important question is simpler:

Do you have a reliable system that converts income into capital every single month?

Before you search for the next opportunity, install the engine.

Before you optimize the portfolio, build the capital base.

Before you chase freedom, respect the sequence.

Income becomes surplus.

Surplus becomes capital.

Capital enters systems.

Systems buy time.

Time creates freedom.

That is Financial Alchemy.

Not motivation.

Not market timing.

Not lifestyle restriction for its own sake.

Transformation.

The transformation of income into capital.

The transformation of capital into systems.

The transformation of systems into freedom.

The Builder stage is not where you stay.

It is where you build the bridge.

And the Surplus Conversion Engine™ is that bridge.

If you are stuck, you are not broken.

You may simply be in the wrong stage with the wrong system.

A correct diagnosis is the beginning of a real solution.

Where are you on the Financial Alchemy path?

Are you still operating as an Earner, trying to stabilize or grow income?

Are you a Builder, creating surplus but struggling to convert it into capital?

Are you an Investor, ready to allocate capital with greater discipline?

Or are you becoming an Owner, building systems that make earning optional?

Take the Financial Alchemy Diagnostic to identify your current stage and discover the highest-leverage system to install next.

Because the goal is not to earn more forever.

The goal is to build systems that eventually make earning optional.

Start with the Diagnostic. Find your stage. Install the right system.